...

If you had read them, you would have seen that the basic theorems of Keynesian economics were discredited and abandoned by 1979 and replaced by other economic theories, and did not come back into any form of use until 2008, and the disastrous economics of the Obama Administration.

...

Apart from proof of being discredited, you only have shown that economists disagree -- hardly a stop the presses moment. Moreover, James Buchanan and Richard Wagner are hardly the final word in economics. Other economists, such as Krugman, Stiglitz and Romer -- as well as Janet Yellen, Ben Bernanke and many others affirm Keynesian thought.

What we learned from Keynes and John Richard Hicks, has actually held up very well in the latest economic crisis. To the extent that we have a crisis in macroeconomics as practiced, it comes from the way many economists chose to reject sensible macro. The truth is nearly the opposite: at least for those economists who didn’t forget Keynes, and understood the IS-LM model. Those economists actually had a very good run, successfully predicting the quiescence of interest rates despite huge budget deficits, the quiescence of inflation despite huge increases in the monetary base, and the adverse effects of harsh austerity policies.

As a response to the Great Depression, American Keynesians said, "We have inadequate demand. Increase government spending!" Almost immediately the economy of the 1930s reversed. So now we came into another great crisis, and again we wanted answers. What would reduce unemployment, and what would make it worse? What effects could we expect from a huge expansion of the Fed’s balance sheet? What about unprecedented peacetime budget deficits? What about austerity programs?

What we saw was that the people who reject Keynes and IS-LM predicting soaring inflation and high interest rates got it wrong, when the Keynesian argued that we had entered a liquidity trap, predicted little effect from the Fed's balance sheet expansion, certainly not an explosion of inflation; low interest rates despite government borrowing; severe adverse effects from austerity. And they were right – because in reality, using a "silly" little model is a lot more sophisticated than talking grandly about complexity, and then trying to make diagnoses with no explicit model at all.

To conclude then that Keynes is "discredited" when it was only the Keynesian economists of today who got it right during the latest crisis while the Austrian economists got it completely wrong, is breathtaking.

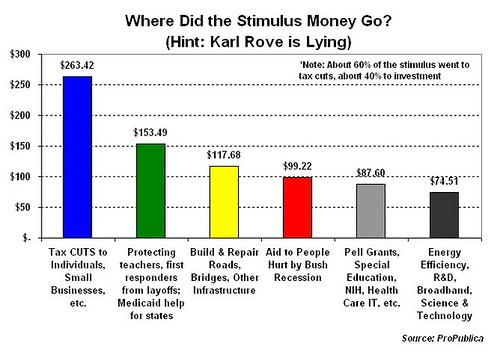

Now, onto you "disastrous economics of the Obama Administration." You should know that the Obama Administration has no effect on monetary policy. To the extent that any president has an effect on the economy, it is in fiscal policy only and that is shared with Congress, who has to pass the president's plan. What, exactly was the disaster? The economy, as measured by GDP, dropped 6-8% a year before Obama was President and employment was dropping by hundreds of thousands of workers per month. Almost immediately upon Obama's stimulus program taking hold, unemployment stopped falling and reversed. In addition, GDP rose.

If there is any criticism of the Obama stimulus, it is that he should have pushed for a bigger stimulus or a second stimulus, as Keynesian economists had argued.

To conclude that the policies of Obama created a disaster has no evidence to support it.