- Joined

- Aug 10, 2013

- Messages

- 20,229

- Reaction score

- 21,622

- Location

- Cambridge, MA

- Gender

- Male

- Political Leaning

- Slightly Liberal

As most folks have probably heard, the Senate has come up with a bipartisan bill (Alexander-Murray) to try and correct some of the artificially-induced issues that exchanges are experiencing right not. It appears to have a filibuster-proof majority--all 48 Democrats + 12 GOP co-sponsors--yet Trump and Ryan have come out in opposition, while McConnell won't allow a vote until Trump is onboard.

The legislation itself is pretty simple. It:

The verdict from the CBO is that the bill will reduce the deficit by $3.8 billion and keep premiums in 2019 lower than they'd be in the absence of the CSRs.

So: should Congress pass this and should the president sign it? Should this bill become law?

The legislation itself is pretty simple. It:

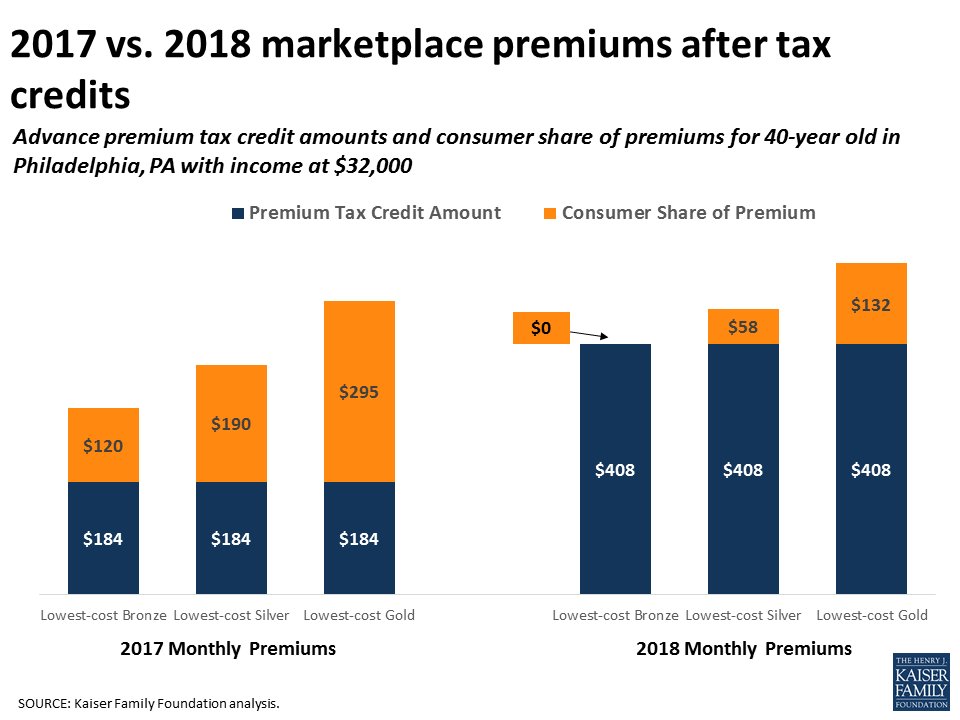

- Appropriates money to fund the cost-sharing reductions (CSRs) that lower deductibles and other out-of-pocket spending for people in the exchanges. Not funding these is estimated to have added ~20% to premium increases for 2018, so this is largely an attempt to undo some of that damage.

- Requires insurers to issue rebates (to consumers and the federal government) of the portion of the artificially-high 2018 premiums that are attributable to the CSRs not being funded.

- Expands access to "copper" plans: catastrophic plans that are less generous (i.e., have higher cost-sharing, like deductibles) than the bronze plans that normally constitute the barest-bones coverage available. Currently only people under 30 and folks who otherwise don't have access to affordable coverage are allowed to buy copper plans; under this bill, any shopper in the individual market could buy one.

- Speeds up the approval process for the ACA's State Innovation Waivers (waivers of the law that allow states to use pass-through money from the ACA to modify the program or try alternatives), with an eye toward encouraging states to set up reinsurance or other risk mitigation programs.

- Restores funding for enrollment outreach that had been cut by the Trump administration.

- Requires HHS to issue regulations implementing the ACA's interstate health compact option (allowing interstate insurance sales).

The verdict from the CBO is that the bill will reduce the deficit by $3.8 billion and keep premiums in 2019 lower than they'd be in the absence of the CSRs.

So: should Congress pass this and should the president sign it? Should this bill become law?