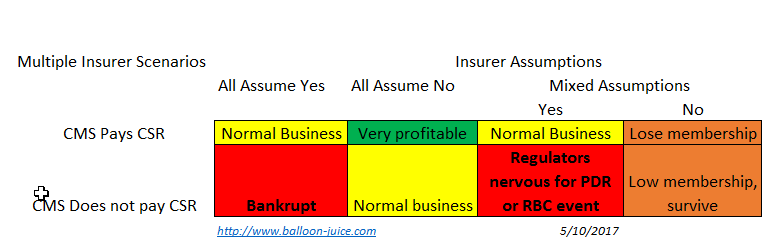

But things get a bit odder when all carriers agree but get the government action wrong. If the carriers think the government will pay but the government does not, the outcomes are unequal. The carrier with the absolute worst value proposition is not hurt that much. No one wants to buy that product anyway. It is a minor hit for an ugly plan.

Now if a insurer offers a very attractively priced plan with a good network and good customer service, they attract all of the membership. That usually is a good thing! Not in this case. Offering the most attractive plan means that plan takes all of the losses. And if that plan goes under, the special enrollment period refugees will choose the next most attractive plan, sending it under. This is an odd winner’s curse scenario.

If there are multiple insurer and they disagree the dynamics are interesting. Insurers that assume they won’t be paid CSR always survive. They won’t get much membership as they are massively overpriced for the market. They will keep some portion of their sickest membership so they will be net risk adjustment recipients and their administrative costs relative to premiums will be very high. But they survive.

In this split decision making scenario, the carriers that are optimistic that CSR will be paid are in an all or nothing scenario. If they are right and the government pays CSR, they get almost all of the membership in the market. Assuming they priced appropriately, they should make good money for the year. If they guess wrong and CSR is not paid, they get all of the membership and the state regulators shut them down due to either a premium deficiency reserve (PDR) event as they have to come up with an extra 20 points of actuarial value that is not being compensated by the government, or there is a risk based capital problem as they have too many members to be safely covered by their current reserves.

But the dynamic changes once all of the optimistic insurers fold, liquidate or withdraw. The surviving insurer(s) will have priced appropriately to handle the special enrollment period refugees from the optimistic insurers. The pessimists will do fine in this scenario.

I am having a hard time seeing (with a strong risk aversion assumption) why a carrier would price on the assumption that CSR will be paid. There is little pay-off and great risk.