Are you asking what the benefit of competition between different actors is?

I'm not in general talking about direct price exposure. In most cases that isn't particularly feasible. More importantly relative price by itself doesn't necessarily tell you what you need to know to make a decision. One of the areas where payers can add value in the future is in using smarter plan designs--i.e., the financial incentives you face in accessing benefits--to provide the choice architecture people need to make decisions. That means where possible encoding the relative value of different providers and treatments into the plan's cost sharing. We've seen some tinkering with tiered networks or value-based insurance design to date but I'd like to see a much more concerted effort to build meaningful signals into the incentives people face.

This can be done in ways that scale to income so that the incentives are there without unduly causing hardship, and certainly they can be done in plans where some part of the premium is subsidized if necessary.

States have turned over most of their Medicaid populations to private insurers. The state pays the insurers a premium for each enrollee, and the insurer is generally responsible for negotiating reimbursements with its provider network. Similar to how things work in the commercial space.

The trend has been distinctly

away from the model you're describing, not towards it. It's possible that Maryland and Vermont's recent all-payer innovations will lead more states into all-payer approaches and perhaps even direct rate-setting but I wouldn't necessarily count on that.

And yet the exchanges have seen more willingness on the part of consumers to defect to competitors than previous public marketplaces. The NYTimes picked up on this back in late '14:

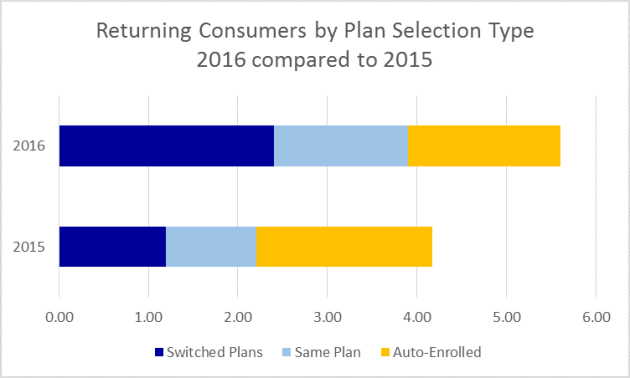

People Are Shopping for Health Insurance, Surprisingly.

That has

held up in subsequent open enrollment periods:

The threat of shoppers voting with their feet is the source of the large degree of price (premium) competition we've seen in the exchanges.

I'm talking exactly about what the exchanges offer. We've seen more price (premium) competition in the exchanges than anticipated, which has put downward pressure on provider prices. When we saw the first-ever drop in hospital prices two years ago, commercial insurance pressures on hospital pricing was one of the main culprits. We've even seen a proliferation of provider-sponsored plans, allowing provider systems to essentially price their suite of services (via a single premium) directly to consumers. There's a reason comparable coverage is significantly cheaper in a competitive exchange than in a non-competitive employer-based plan.

The point of moving more people from the less-competitive private insurance space that's ~14 times bigger by enrollment and into more competitive marketplaces is not simply to "change the lineup of plan offerings," it's to spread the incentives encouraging cost containment to the rest of the market. Really make the exchanges market-movers and you'll see that greater enrollment doesn't simply make them more stable and more attractive to potential sellers, the managed care competition for the most favorable provider contracts will be significant.

")