- Joined

- Dec 20, 2009

- Messages

- 75,763

- Reaction score

- 40,018

- Location

- USofA

- Gender

- Male

- Political Leaning

- Conservative

Once again, slip sliding into that wonderful little set of economic conditions that the keyensians swear can't happen..... but here we are.

gosh. who could have forseen this? who could have possibly known that having the government take away massive resources from the productive sectors in society and pour it into the unproductive sectors would reduce growth? who could have ever been able to predict that the Fed would never be able to pull all that money back in like it had dumped it out? surely nobody knew that weakening the US dollar would cause an eventual sell off overseas.

oh wait. oh yeah that's right. Glenn Beck. and everyone else who knows how to read a history book.

Glenn Beck. and everyone else who knows how to read a history book.

sooooo..... all you "deflation" hawks, again. we told you so.

it's like Niall Ferguson said. Barack Obama is just the new Jimmy Carter.

oh wait, that's right. we predicted that, too.... back in 2008.

but hey, maybe the people will be fooled, eh? maybe the Fed will just keeeeep buying those bonds, we can keep interest rates low juuuust long enough, and we can just hold the whole thing together through 2012 for reelection, eh?

huh, nope.

gosh. who could have forseen this? who could have possibly known that having the government take away massive resources from the productive sectors in society and pour it into the unproductive sectors would reduce growth? who could have ever been able to predict that the Fed would never be able to pull all that money back in like it had dumped it out? surely nobody knew that weakening the US dollar would cause an eventual sell off overseas.

oh wait. oh yeah that's right.

Glenn Beck. and everyone else who knows how to read a history book.sooooo..... all you "deflation" hawks, again. we told you so.

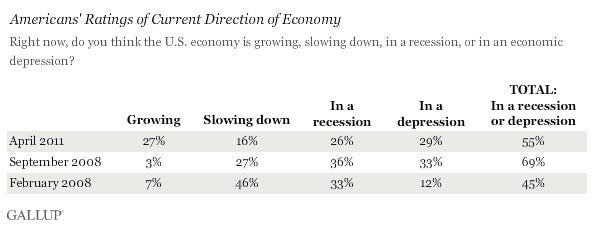

Stagflation officially returned today with a nasty GDP report that showed only 1.8 percent real growth, but 3.8 percent for the consumer spending deflator. It’s a mini version of the 1970s: low growth, higher inflation.

Looked at another way, rising inflation is coexisting with high, near-9 percent unemployment. Keynesians argue this can’t happen. They believe strong growth and too many people working leads to high inflation. But they were blown out of the water way back in the ’70s. And their view is hitting another pothole right now....

U.S. economic growth slowed more than expected in the first quarter as higher food and gasoline prices dampened consumer spending, and sent a broad measure of inflation rising at its fastest pace in 2-1/2 years....

The Federal Reserve on Wednesday acknowledged the slowdown in first-quarter growth, describing the recovery as proceeding at a "moderate pace"—a slight step back from a statement in March when it said the economy was on a "firmer footing."

It trimmed its growth estimate for 2011 to between 3.1 and 3.3 percent from a 3.4 to 3.9 percent January projection.

The U.S. central bank signaled it was in no rush to start withdrawing the massive monetary stimulus it has lent the economy. It confirmed plans to complete its $600 billion bond buying program in June....

it's like Niall Ferguson said. Barack Obama is just the new Jimmy Carter.

oh wait, that's right. we predicted that, too.... back in 2008.

but hey, maybe the people will be fooled, eh? maybe the Fed will just keeeeep buying those bonds, we can keep interest rates low juuuust long enough, and we can just hold the whole thing together through 2012 for reelection, eh?

huh, nope.