- Joined

- Dec 13, 2015

- Messages

- 9,594

- Reaction score

- 2,072

- Location

- France

- Gender

- Male

- Political Leaning

- Centrist

From the Economist: Business in America: Too much of a good thing

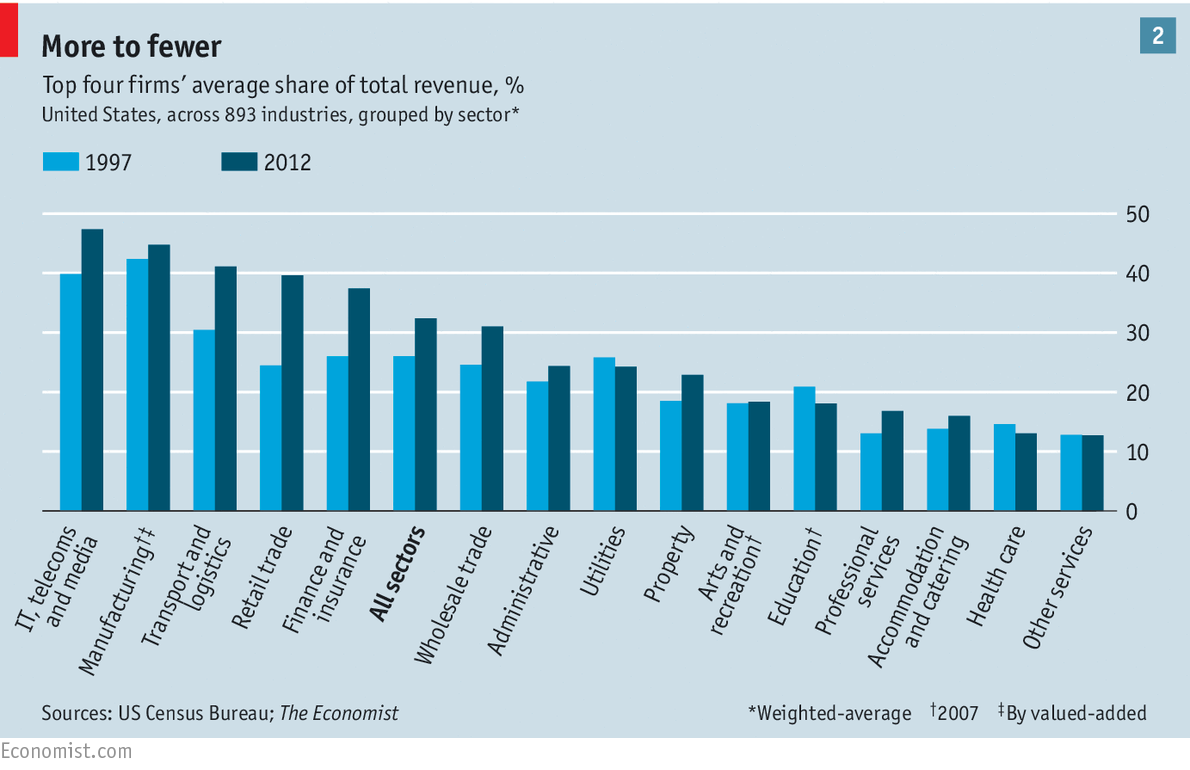

We may like to think the US markets are a competitive jungle ("survival of the fittest" and all that), but that is not what has been happening in the past 30/40 years as mega-mergers have consolidated markets. Typically, nowadays, there are 2, 3, or four main marketeers who dominate the market and a handful of "also rans". One of the biggest-in-the-making is Amazon.

See here:

The lack of market competitiveness simply means that the consumers pay more because of the lack of real competition. Product niches are made to all "look alike" and their differentiation in the mind of the consumer has been drastically lessened. Price differentials are minimal thus underlining the contention that market-competition is practically non-existant.

Excerpted from the above linked Economist article:

We may like to think the US markets are a competitive jungle ("survival of the fittest" and all that), but that is not what has been happening in the past 30/40 years as mega-mergers have consolidated markets. Typically, nowadays, there are 2, 3, or four main marketeers who dominate the market and a handful of "also rans". One of the biggest-in-the-making is Amazon.

See here:

The lack of market competitiveness simply means that the consumers pay more because of the lack of real competition. Product niches are made to all "look alike" and their differentiation in the mind of the consumer has been drastically lessened. Price differentials are minimal thus underlining the contention that market-competition is practically non-existant.

Excerpted from the above linked Economist article:

Profits are an essential part of capitalism. They give investors a return, encourage innovation and signal where resources should be invested. Their accumulation allows investment in bold new ventures. Countries where profits are too low—Japan, for instance—can slip into morbid torpor. Firms that ignore profits, such as China’s state-run enterprises, lurch around like aimless zombies, as likely to destroy value as to create it.

But high profits across a whole economy can be a sign of sickness. They can signal the existence of firms more adept at siphoning wealth off than creating it afresh, such as those that exploit monopolies. If companies capture more profits than they can spend, it can lead to a shortfall of demand. This has been a pressing problem in America. It is not that firms are under investing by historical standards. Relative to assets, sales and GDP, the level of investment is pretty normal. But domestic cash flows are so high that they still have pots of cash left over after investment: about $800 billion a year.

High profits can deepen inequality in various ways. The pool of income to be split among employees could be squeezed. Consumers might pay too much for goods. In a market the size of America’s prices should be lower than in other industrialised economies. By and large, they are not. Though American companies now make a fifth of their profits abroad, their naughty secret is that their return-on-equity is 40% higher at home.

Most explanations of America’s high profits draw on national-accounts data which show that the fall in the share of output going to workers over the past decade is equivalent to about 60% of the rise in domestic pre-tax profits. Scholars typically have three explanations for this: technology, which has allowed firms to replace workers with machines and software; globalisation, which has made it easier to shift production to lower cost countries; and a decline in trade-union membership.

None of these accounts, though, explain the most troubling aspect of America’s profit problem: its persistence. Business theory holds that firms can at best enjoy only temporary periods of “competitive advantage” during which they can rake in cash. After that new companies, inspired by these rich pickings, will pile in to compete away those fat margins, bringing prices down and increasing both employment and investment. It’s the mechanism behind Adam Smith’s invisible hand.

In America that hand seems oddly idle. An American firm that was very profitable in 2003 (one with post-tax returns on capital of 15-25%, excluding goodwill) had an 83% chance of still being very profitable in 2013; the same was true for firms with returns of over 25%, according to McKinsey, a consulting firm. In the previous decade the odds were about 50%. The obvious conclusion is that the American economy is too cosy for incumbents.

Last edited: