Well, that was the scam...

In 1991, the Glass–Steagall Act was repealed, originally, the crimes that the Glass-Stiegall act prevented were acts that the founding fathers would have considered an act of the same magnitude as treason... but the most important part is that this allows for 'derivatives investments'... where the 'value' derives from the value of something else.

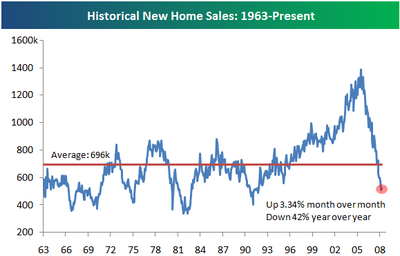

Since then big banks have formed, and they make mortgages they KNOW people can't pay back so that they get MASSIVE volume of loans, and creates an artificial bubble because most of these people should at best be renting. That's the setup... and this is the only area where there's individual fraud on top of corporate fraud.

Here's where it gets fun... because each bank might be holding hundreds of thousands or millions of these mortgages, they create a 'pool' on which people can invest in these 'mortgage backed securities'. They convince the regulators that these are all AAA investments when the reality is that they are only as good, but they are a mix of good and bad. Overtime, the banks learn the good from the bad, and sell the good to their friends and the bad to anyone else... and split them off and since more people are invested the regulators effectively get bought off to continue rating these at AAA.

So, when a person defaults on the mortgage, well, they are not defaulting on a 100 000 $ house... they are killing that investment holding that mortgage... and since these are leveraged at 100:1 (I'm told, correct me if wrong) that 1 house kills off a 10 million dollar share of the overall stock.

So, your '5.2 trillion' COULD actually be the base on which exist this leveraged investments... MEANING... that 5.2 trillion is 0.5 QUADRILLION. This is all bank debts for creating this ponzi scheme...

Here's the final nail :

Bailout of these derivatives. Put that on tax payer heads, and it doesn't matter what the interest is, there's not that much that can be produced on earth through which you can pay that debt...