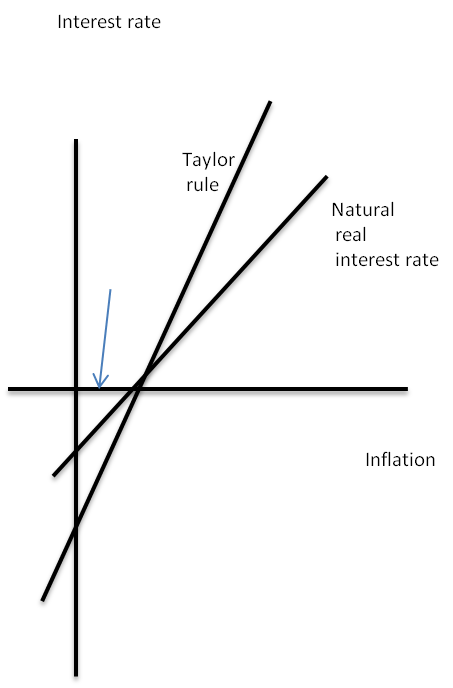

with the blue arrow pointing to our current position. We got here, of course, thanks to a huge financial shock that shifted the natural real interest rate way down. Now, at this point any Taylor rule fitted to past Fed behavior says that the Fed funds rate should be something like minus 5 or 6 right now, but you can’t do that, so we’re stuck with an interest rate that’s too high given low inflation and very high unemployment.

The crucial thing to understand about this position is that it’s not self-correcting. On the contrary, as inflation falls over time and possibly goes to actual deflation, we sink deeper into the trap.

That’s why the Fed’s wait-and-see policy is so wrong-headed: to the extent that the Fed thinks it can use unconventional measures to get some traction, it should use them now now now, not wait until expectations of below-target inflation have gotten embedded.

It’s also why fiscal policy should have been much more aggressive than it was; even aside from the political dynamics, which said that we’d only get one shot, the economic dynamics also said that not doing enough early on only makes an eventual solution harder.

The sad thing is that policy makers were supposed to know all this. The Fed had studied Japan extensively, and believed that the Bank of Japan could have averted the lost decade if it had reacted very aggressively early on. Larry Summers talked about a Powell doctrine of overwhelming force in the face of crisis. And yet what we actually got was an underpowered response on both the fiscal and the monetary fronts.