Actually, I'd say it is "whoever has the best idea."

Unfortunately, turning TANF into block grants for the states indicates that state control isn't necessarily the best idea (

How States Have Spent Federal and State Funds Under the TANF Block Grant — Center on Budget and Policy Priorities).

Also, few municipalities (aside from big urban centers) have the resources to really deal with providing safety nets, let alone designing them to avoid welfare traps.

I've said several times in this thread that I don't blame Bush much for the bubbles. He had a little bit of responsibility, as did Clinton; both of them failed to uphold or implement regulations that would have reduced the contagion, though neither really could have eliminated the bubble. Greenspan had more responsibility, since low interest rates were one factor, and Greenspan held a hard line against any financial or mortgage regulations.

The banks bear more responsibility than the politicians. To make a long story short: There was a ton of capital (US and international) looking for a home, and the Dot Com implosion shifted capital away from equities and into real estate. Real estate rarely has a multi-regional decline; in most cases, one region will decline while others do fine. So, money starts pouring into real estate.

New financial innovations wound up pouring tons of fuel on the fire. Mortgage brokers misused risk modeling software, which masked the risks. Mortgage originators started selling mortgages to Wall Street, and had no incentives or requirements to hold onto any of the mortgages, so they had no skin in the game. Wall Street banks used CDOs and MBSs to slice and dice the mortgages, which increased the obscurity and disguised the risks, and also resulted in the banks not caring if the borrowers defaulted. Not only did the banks shovel the derivatives at an uneducated market, they also in some cases bet against their own products with CDS's.

It is important to note that while CDOs can be a good product, they were certainly abused by the investment banks. The entire structure was flawed; the top-rated tranches were not typically specified based on the risks of the mortgages, but

who gets paid first. Some banks would also take the lowest (riskiest) tranches, repackage them into another CDO to further obscure the risks. Other products like synthetic CDOs were so complex that I don't know why anyone would buy them.

Another factor is that banks abused their own VAR systems, and failed to assess the risks to their own existence. They also heavily pressured the ratings agencies to give their products higher ratings than they deserved, with the threat of pulling business (talk about a flawed incentive system).

Of course, none of this works without buyers, of both the homes and the derivatives. Lots of people bought homes they knew, or should have known, they couldn't have afforded. Investors bought financial products they didn't fully understand, which is never a good idea.

Subprime was as much a symptom than a cause. They only really became a big force well into the bubble, when the mortgage brokers and banks were running out of borrowers with decent credit histories and decent jobs. In 2003, subprimes were still only 8% of the market; it leaped to 18% in 2004, then 20% in 2005 and 2006. There were also lots of issues with option ARMs, interest-only mortgages, 80-20s and so forth:

So yeah, the banks do hold a fair amount (if not the bulk) of responsibility for the crisis and subsequent recession, and were not sufficiently taken to task yet for their role.

Not only are my personal affairs none of your business, my own experiences have nothing to do with how the bubble formed, perpetuated and burst.

Because they're distorting both the political system and the economy, and some of the choices they're making have a negative effect on the entire country.

Again, it's not about me.

What they do that potentially harms the entire economy is that some of the super-wealthy want to cut functions that are critical for the nation as a whole (e.g. education, regulation, safety nets). Their enormous wealth also gives them significantly more influence over politicians, via contributions and lobbying -- now more than ever, since the SCOTUS unleashed nearly-unlimited campaign spending.

*sigh* Again, since you repeatedly insist on excluding SS and Medicare, it's a $2.5 trillion projected deficit for 2015.

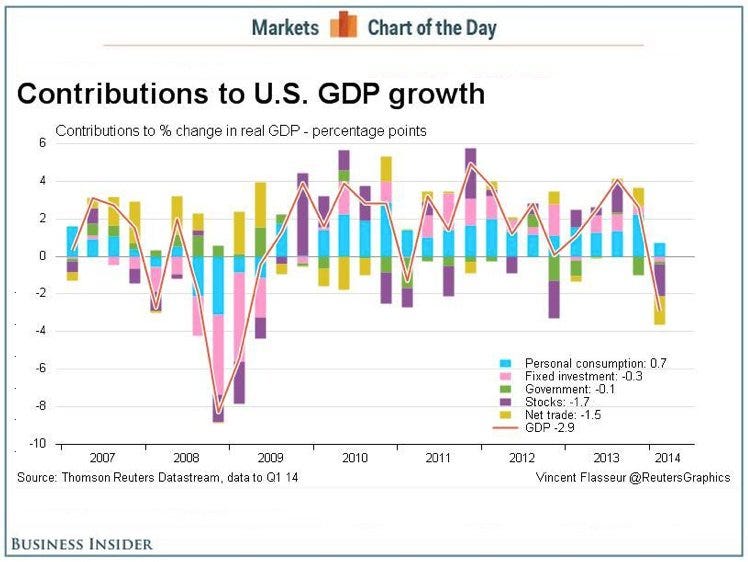

I never said "I don't care about waste." In fact, we haven't really discussed waste very much. The topic of this thread is the slightly ridiculous claim that one quarter of negative growth is somehow supposed to be an indicator that the entire economy is going down the tubes, which is not the case.

So, to that end: Government spending, revenue collections, high deficits and high debt actually are not a problem for the US economy. Deficits are roughly back in line from the past ~40 years. Despite a slow grinding recovery, things

are getting better, so debt as a percentage of GDP

is likely to fall, especially if we cut defense spending to a reasonable level and keep health care spending in check. In the short and medium term, the US is more than capable of paying what it owes, and the funds it's using are not a detriment at a time when lenders are still reluctant to lend.