Bush drive for home ownership fueled housing bubble

By Jo Becker, Sheryl Gay Stolberg and Stephen Labaton

Published: Sunday, December 21, 2008

WASHINGTON — "We can put light where there's darkness, and hope where there's despondency in this country. And part of it is working together as a nation to encourage folks to own their own home."

- President George W. Bush, Oct. 15, 2002

The global financial system was teetering on the edge of collapse when Bush and his economics team huddled in the Roosevelt Room of the White House for a briefing that, in the words of one participant, "scared the hell out of everybody."

It was Sept. 18. Lehman Brothers had just gone belly-up, overwhelmed by toxic mortgages. Bank of America had swallowed Merrill Lynch in a hastily arranged sale. Two days earlier, Bush had agreed to pump $85 billion into the failing insurance giant American International Group.

The president listened as Ben Bernanke, chairman of the Federal Reserve, laid out the latest terrifying news: The credit markets, gripped by panic, had frozen overnight, and banks were refusing to lend money.

Then his Treasury secretary, Henry Paulson Jr., told him that to stave off disaster, he would have to sign off on the biggest government bailout in history. Bush, according to several people in the room, paused for a single, stunned moment to take it all in.

"How," he wondered aloud, "did we get here?"

Eight years after arriving in Washington vowing to spread the dream of home ownership, Bush is leaving office, as he himself said recently, "faced with the prospect of a global meltdown" with roots in the housing sector he so ardently championed.

There are plenty of culprits, like lenders who peddled easy credit, consumers who took on mortgages they could not afford and Wall Street chieftains who loaded up on mortgage-backed securities without regard to the risk.

But the story of how the United States got here is partly one of Bush's own making, according to a review of his tenure that included interviews with dozens of current and former administration officials.

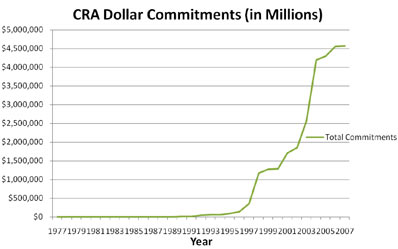

From his earliest days in office, Bush paired his belief that Americans do best when they own their own homes with his conviction that markets do best when left alone. Bush pushed hard to expand home ownership, especially among minority groups, an initiative that dovetailed with both his ambition to expand Republican appeal and the business interests of some of his biggest donors. But his housing policies and hands-off approach to regulation encouraged lax lending standards.

Bush did foresee the danger posed by Fannie Mae and Freddie Mac, the government-sponsored mortgage finance giants. The president spent years pushing a recalcitrant Congress to toughen regulation of the companies, but was unwilling to compromise when his former Treasury secretary wanted to cut a deal. And the regulator Bush chose to oversee them - an old school buddy - pronounced the companies sound even as they headed toward insolvency.

As early as 2006, top advisers to Bush dismissed warnings from people inside and outside the White House that housing prices were inflated and that a foreclosure crisis was looming. And when the economy deteriorated, Bush and his team misdiagnosed the reasons and scope of the downturn. As recently as February, for example, Bush was still calling it a "rough patch."

The result was a series of piecemeal policy prescriptions that lagged behind the escalating crisis.

...