- Joined

- Sep 29, 2007

- Messages

- 29,262

- Reaction score

- 10,126

- Gender

- Undisclosed

- Political Leaning

- Undisclosed

Insurance premiums are going up, employee plans are going up to the companies, this is only the beginning. If it makes you feel better that it's only 14 cents increase for one item(that is visible, not counting other cost increases) before the entire turd has started to smell then I don't know what to tell you Deuce. The bill isn't even fully implemented until 2016 and it is constantly able to be changed without congressional input through the NHS, these are initial increases. So, .14$ for a pizza, 120$ for a Ford, .30$ for a gallon of gas, it adds up.

I'd take what we have now over:

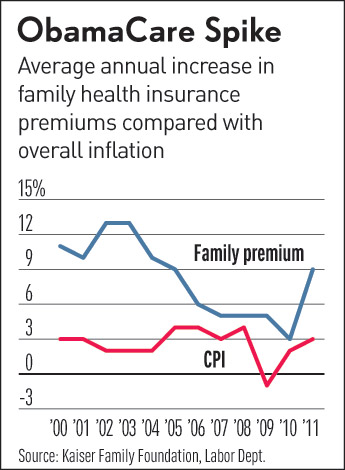

In 2008, the average annual premiums for

employer-sponsored health insurance are

$4,704 for single coverage and $12,680

for family coverage, up about 5% from

the 2007 average premiums.

2

Since 1999,

average premiums for family coverage

have increased 119% (Exhibit A). Average

premiums for family coverage are lower for

workers in small firms (3–199 workers)

than for workers in large firms (200 or

more workers). Premiums are higher

in self-funded plans than fully insured

plans for single and family coverage.

Average premiums for HDHP/SOs are

lower than the overall average for all plan

types for both single and family coverage

(Exhibit B).

http://ehbs.kff.org/images/abstract/7791.pdf

")