For Social Security this is not correct - there are more payers than recipients.

...no. Firstly, we peg the growth in COLA to inflation, rather than wages, meaning that we are reducing Social Security's scheduled payouts to everyone, including the housewives etc. A second reduction in payouts comes from the accounts of those who are wage-earners, which is the vast majority of recipients.

Which part?

")

I've put up quite a lot throughout the thread.

Younger workers make less and older workers make more - remember that what we are looking at here is people retiring at different times, and the younger/lowerincome folks are (see OP) actually better situated than the older/higher income folks because their long term return is better. If your typical 28 year old is making $38,000 today, then that's more than fine because it means that (assuming a RIO of 7.5% and a growth in income of 2%, commensurate with what Social Security currently assumes) he will have completely replaced what the government would have been on the hook for by the time he reaches about age 50. So he's a lower income worker, yes. Who now represents zero liability to social security. Since the

vast majority of low income earners are in that age bracket, and since the average income of the 15-24 year old age bracket is about

$14,539; they have a fairly heavy pull on national averages.

So (as of 2012), full time workers had an average income of

$59,532 (median $45,365), which cuts out the part-timers that are going to be heavily represented in that 15-24 year old lower-income age bracket.

So a relevant bit to bring in is household income by age bracket:

And you'll see the same trend repeated - the older workers have greater experience and skill sets, and tend to earn more, until they start retiring (it seems we like to retire early - boomers are all getting out asap), at which point they earn less.

The point being that the very workers who represent the largest loss in revenue from their 10% FICA, A) current figures do not depend on much more income from them, making the loss the least over time and B) they are most likely to most heavily mitigate through replacement of the benefit from their accounts.

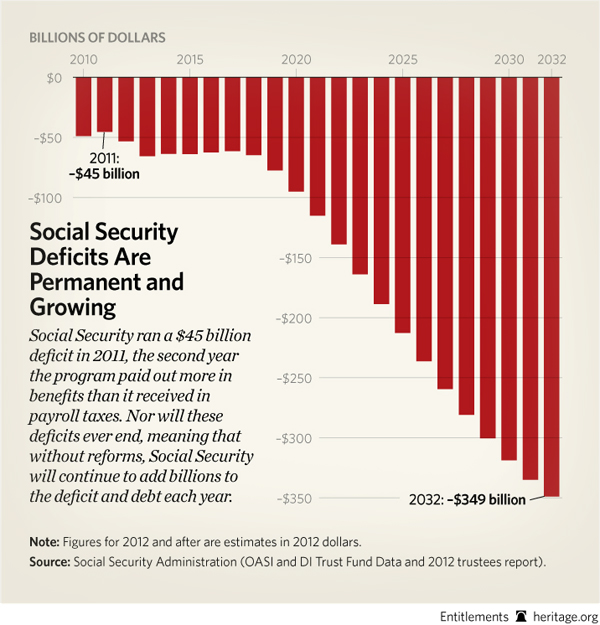

Social Security deficits are sustainable for a short time:

This is about where we are currently sitting. By popping the cap and indexing growth to inflation instead of wages, we reduce the near-year deficits by about 85%, before we reduce FICA inputs to put the deficits back up. By the time we get to that 2032 year mark, by my count, the

average retiree should be replacing somewhere around 75% of his SS check,

significantly reducing necessary outlays instead of collapsing the system. When the first private-account-retirees start dying, as well, an additional 50% of their account is taxed right back into SS.

I wouldn't be averse to additionally flattening the benefit by ending or sharply reducing COLA increases for upper-income retirees, similar to the Simpson-Bowles Proposal:

But only if necessary to make the thing solvent.