P I S A

Rather, I suggest, is that they should not be. And that is a matter of primary/secondary schooling for the ability to make basic calculations and logical assumptions.

But if you are not, who's fault is it - the schooling or yourself? I say its preponderantly the former. In general, humans are not born dumb. But they certainly can be made dumb. Howzat?

It depends upon external influences in the Learning Process. (And here the BoobTube clearly is a factor.) Meaning, in the formation of the individual, little is more important than Education.

And in that matter, the US is fairly mediocre as regard primary/secondary schooling. Whyzat?

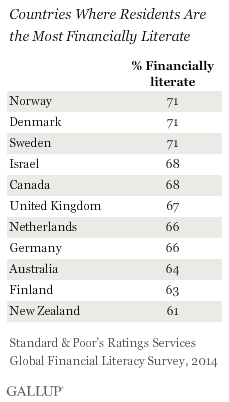

Consider the results of the OECD's PISA program. (No, it has nothing whatsoever to do with that delightful town in Italy.) PISA = Program for International Student Assessemt - which tests secondary school levels in the OECD countries on a systematic basis. Students across the 64 countries are tested upon Reading, Writing and Science.

Here are the Key PISA 2012 Findings for the US (sourced from

here):

"Key findings

• Among the 34 OECD countries, the United States performed below average in mathematics in

2012 and is ranked 27th (this is the best estimate, although the rank could be between 23 and

29 due to sampling and measurement error). Performance in reading and science are both

close to the OECD average. The United States ranks 17 in reading, (range of ranks: 14 to 20)

and 20 in science (range of ranks: 17 to 25). There has been no significant change in these

performances over time.

• Mathematics scores for the top-performer, Shanghai-China, indicate a performance that is the

equivalent of over two years of formal schooling ahead of those observed in Massachusetts,

itself a strong-performing U.S. state.

•

While the U.S. spends more per student than most countries, this does not translate into

better performance. For example, the Slovak Republic, which spends around USD 53 000 per

student, performs at the same level as the United States, which spends over USD 115 000 per

student.

• Just over one in four U.S. students do not reach the PISA baseline Level 2 of mathematics

proficiency – a higher-than-OECD average proportion and one that hasn’t changed since 2003. At

the opposite end of the proficiency scale, the U.S. has a below-average share of top performers.

•

Students in the United States have particular weaknesses in performing mathematics tasks with

higher cognitive demands, such as taking real-world situations, translating them into mathematical

terms, and interpreting mathematical aspects in real-world probleMS. An alignment study between

the Common Core State Standards for Mathematics and PISA suggests that a successful

implementation of the Common Core Standards would yield significant performance gains also in

PISA.

• Socio-economic background has a significant impact on student performance in the United

States, with some 15% of the variation in student performance explained by this, similar to

the OECD average. Although this impact has weakened over time,

disadvantaged students

show less engagement, drive, motivation and self-beliefs.

• Students in the U.S. are largely satisfied with their school and view teacher-student relations

positively. But they do not report strong motivation towards learning mathematics: only 50%

of students agreed that they are interested in learning mathematics, slightly below the OECD

average of 53%."

Next, consider the ranking of the US amongst the OECD country members

here. (Scroll down to page 5.)

I'll save you the counting: The US is in 36th position of all 64 countries.

We can do one helluva lot better. The only question is, How?